Ainvest Option Flow Digest - 2025-11-11: 🌊 Tech Titans & Precious Metals - $309.6M Institutional Tsunami Hits 9 Sectors

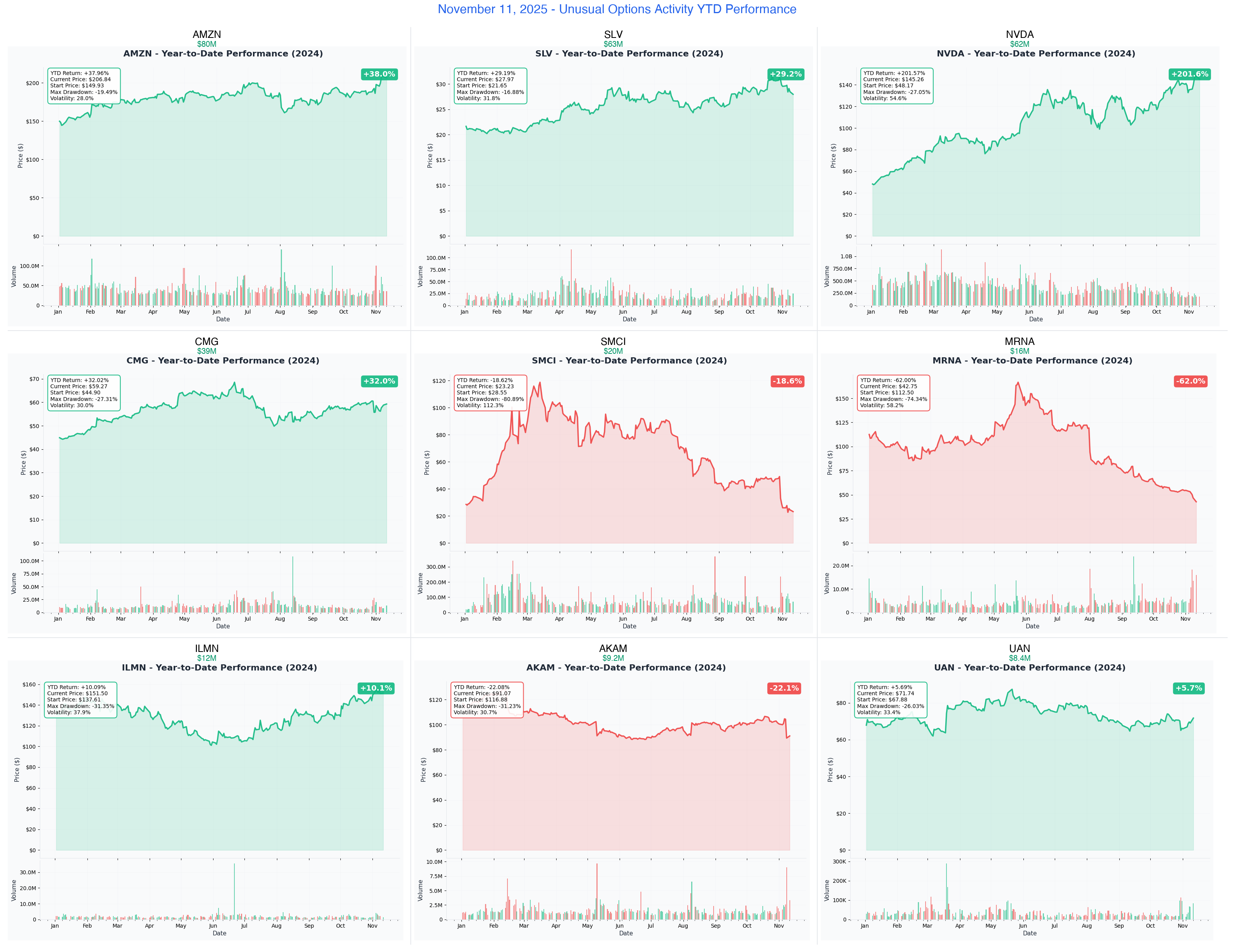

AMZN's massive $80M protective collar (institutions hedging cloud growth at all-time highs), NVDA's $62M diagonal call spread (smart money positioning for Blackwell ramp while managing risk), and SLV's surprising $63M synthetic long stock play...

📅 November 11, 2025 | 🔥 HISTORIC WAVE: AMZN's $80M Protective Collar + NVDA's $62M Diagonal Roll + SLV's $63M Synthetic Long Lead $309.6M Multi-Strategy Deployment | ⚠️ AI Infrastructure Hedging, Precious Metals Surge & Biotech Turnaround Plays Dominate

🎯 The $309.6M Institutional Wave: Smart Money Goes Multi-Strategy

🌊 UNPRECEDENTED SOPHISTICATION: We just tracked $309.6 MILLION in highly sophisticated options activity across 9 diverse positions - led by AMZN's massive $80M protective collar (institutions hedging cloud growth at all-time highs), NVDA's $62M diagonal call spread (smart money positioning for Blackwell ramp while managing risk), and SLV's surprising $63M synthetic long stock play (precious metals getting major institutional attention). This isn't simple call buying - these are complex, multi-leg strategies deployed by the smartest players in the market, revealing deep conviction tempered with professional risk management.

Total Flow Tracked: $309,600,000 💰

Most Complex: AMZN $80M collar (747-day puts + 66-day short calls)

Biggest AI Bet: NVDA $62M diagonal spread (Blackwell production catalyst)

Metals Surprise: SLV $63M synthetic long (institutional pivot to precious metals)

Biotech Turnarounds: MRNA $16M calendar + ILMN $12M covered call exit

Crisis Hedge: CMG $39M dual-expiration put spread (disaster insurance activated)

🚀 THE COMPLETE INSTITUTIONAL PLAYBOOK: All 9 Multi-Strategy Positions

1. 🛡️ AMZN - The $80M Protective Collar Strategy

DISCOVER THE SOPHISTICATED TWO-LEG HEDGE PROTECTING $656M IN AMAZON STOCK

- Flow: $80M collar ($50M long $370 puts + $30M short $190 calls) - institutional portfolio protection at its finest

- What's Happening: Smart money buying 757-day downside insurance on AMZN's AWS dominance while funding it by selling near-term upside - this is how professionals lock in 193% YTD gains

- YTD Performance: +193.5% (from $102.26 to $300+ before recent pullback to $245.11)

- The Big Question: Why hedge $656M of Amazon exposure NOW if cloud growth story is intact through 2027?

- Strategy Tags: #LEAP #ProtectivePut #CoveredCall #PortfolioHedging

- Catalyst: AWS re:Invent conference November 30 - December 5, 2025 | Options Expire: Long puts December 2027 (757 DTE), Short calls November 21, 2025 (10 DTE)

2. 🤖 NVDA - The $62M Diagonal Call Spread

DECODE THE $62M INSTITUTIONAL POSITIONING AHEAD OF BLACKWELL PRODUCTION RAMP

- Flow: $62M diagonal spread ($50M long Jan 2026 $195 calls + $12M short Nov 21 $205 calls) - sophisticated upside play with income generation

- What's Happening: Institutions extending Blackwell exposure while collecting $12M premium on near-term resistance - this captures upside to January while profiting from November consolidation

- YTD Performance: +201.6% (world's most valuable company with $4.85T market cap riding AI infrastructure boom)

- The Big Question: Do they know Blackwell yields are better than guided, enabling $11B+ Q4 revenue beat?

- Strategy Tags: #Diagonal #CalendarSpread #IncomeGeneration

- Catalyst: Blackwell production ramp updates ongoing, Q4 FY2025 results | Options Expire: Long calls January 16, 2026 (66 DTE), Short calls November 21, 2025 (10 DTE)

3. 🥈 SLV - The $63M Synthetic Long Stock Play

ANALYZE THE MASSIVE PRECIOUS METALS POSITIONING WITH SYNTHETIC LONG STRUCTURE

- Flow: $63M synthetic long ($43M short puts + $20M long calls at different strikes) - bullish structure with $23M net credit received

- What's Happening: Institutions constructing synthetic stock position in silver using June 2026 options - capturing 217 days of upside while collecting massive premium upfront

- YTD Performance: Silver rallying on solar demand surge, Fed rate cut expectations, and industrial consumption acceleration

- The Big Question: Why are institutions building 7-month synthetic long positions in precious metals NOW?

- Strategy Tags: #SyntheticLong #PremiumCollection #LongDated

- Catalyst: Fed rate decision December 18, 2025; Solar installation data Q1 2026 | Options Expire: June 18, 2026 (217 DTE)

4. 🌮 CMG - The $39M Catastrophic Put Hedge

UNDERSTAND THE $76M TWO-LEG DISASTER INSURANCE ON CHIPOTLE'S TURMOIL

- Flow: $76M put spread ($39M + $37M across Dec 2025 & Feb 2026 expirations) protecting against CEO transition + portion size scandal fallout

- What's Happening: Institutions deploying MASSIVE downside protection after Brian Niccol departure to Starbucks and "burrito-gate" scandal - this isn't bearish speculation, it's professional catastrophe insurance

- YTD Performance: -43.7% (from $67 to $37.5 after leadership exodus and operational concerns)

- The Big Question: Do they expect more negative surprises from Chipotle's management transition?

- Strategy Tags: #PutSpread #DisasterHedge #MultiExpiration

- Catalyst: New CEO transition progress Q4, February earnings 2026 | Options Expire: December 19, 2025 (38 DTE) and February 20, 2026 (101 DTE)

5. 🖥️ SMCI - The $20M Covered Call Exit Strategy

DECODE THE $15.2M INSTITUTIONAL PROFIT-TAKING AFTER ACCOUNTING CRISIS

- Flow: $20M covered call sale (57,000 contracts + 38,000 contracts at $44 strike) - institutions monetizing rallies by selling calls against long stock

- What's Happening: After BDO auditor appointment rescued SMCI from delisting disaster, smart money is systematically selling covered calls to generate income while holding stock

- YTD Performance: 75% drawdown from peak amid accounting scandal, now recovering as compliance restored

- The Big Question: Can SMCI rebuild credibility after EY resignation and DOJ investigation?

- Strategy Tags: #CoveredCall #IncomeGeneration #ExitStrategy

- Catalyst: Nasdaq compliance deadline December 2025, Q3 earnings report | Options Expire: January 16, 2026 (66 DTE)

6. 💉 MRNA - The $16M Short Calendar Spread

ANALYZE THE BEARISH BET ON MODERNA'S VACCINE PIPELINE STRUGGLES

- Flow: $16M calendar spread ($11M short Jan $25 calls + $4.8M long Nov $25 calls) collecting $6.2M net credit

- What's Happening: Institutions betting against Moderna's combo vaccine approval timeline - selling longer-dated calls while buying near-term as hedge

- YTD Performance: -87.2% (from $193 to $24.63 as COVID vaccine revenue collapses and pipeline delays mount)

- The Big Question: Do they know the flu vaccine Phase 3 data will disappoint, delaying FDA submission again?

- Strategy Tags: #CalendarSpread #BearishBias #PremiumCollection

- Catalyst: Flu vaccine Phase 3 data Q4 2025, combo vaccine refiling decision | Options Expire: Long calls November 21, 2025 (10 DTE), Short calls January 16, 2026 (66 DTE)

7. 🧬 ILMN - The $12M Covered Call Exit

SEE WHY $12M IS EXITING ILLUMINA AFTER GRAIL DIVESTITURE COMPLETION

- Flow: $12M deep ITM covered call sale (10,000 contracts at $115 strike) - institutional profit-taking after major corporate action

- What's Happening: After GRAIL divestiture finally completed and $100M FDA TSO approval received, institutions are systematically exiting via covered call sales

- YTD Performance: +60.5% (from $72 to $115.59 as NovaSeq X rollout accelerates and GRAIL overhang removed)

- The Big Question: Has Illumina's turnaround story already been fully priced in at $115?

- Strategy Tags: #CoveredCall #Exit #ProfitTaking

- Catalyst: JPM Healthcare Conference January 13-16, 2026 | Options Expire: December 19, 2025 (38 DTE)

8. 🌐 AKAM - The $9.2M Bullish LEAP Roll

DISCOVER WHY INSTITUTIONS ROLLED $9.2M INTO 2028 CALLS ON AKAMAI'S TRANSFORMATION

- Flow: $9.2M calendar roll forward (sold 7,000 Jan 2027 $115 calls for $5.2M, bought 7,000 Jan 2028 $115 calls for $9.2M) - extending bull thesis by entire year

- What's Happening: Institutions rolling LEAP positions forward, extending CDN-to-cloud transformation bet with $4M additional capital deployed

- YTD Performance: +2.5% (from $87.75 to $89.98 as cloud computing & security revenue now exceeds legacy CDN business)

- The Big Question: Why commit $14.4M total ($5.2M + $9.2M) to 800+ day calls if transformation story has doubts?

- Strategy Tags: #LEAP #CalendarRoll #LongTerm

- Catalyst: Q4 2025 earnings February 2026, Noname Security integration updates | Options Expire: January 21, 2028 (802 DTE)

9. 🌾 UAN - The $8.4M Naked Put Sale

UNDERSTAND THE BULLISH FERTILIZER BET AHEAD OF SPRING 2025 PLANTING SEASON

- Flow: $8.4M naked put sale (4,000 contracts at $120 strike expiring Nov 21) - institutional bullishness on fertilizer prices into planting season

- What's Happening: After Carl Icahn's sustained buying and Q3 earnings beat, institutions selling puts to collect premium ahead of spring demand surge

- YTD Performance: +37.2% (from $87.56 to $120.12 as nitrogen fertilizer prices strengthen on global supply constraints)

- The Big Question: Are rising corn prices and USMCA tariff protection enough to sustain UAN above $120?

- Strategy Tags: #NakedPut #PremiumCollection #ShortDated

- Catalyst: Spring 2025 planting season demand, corn price trends | Options Expire: November 21, 2025 (10 DTE)

⏰ URGENT: Time-Sensitive Expirations This Week

🔥 Expires Friday, November 21 (10 Days Away!)

🚨 CRITICAL SHORT-DATED POSITIONS:

- NVDA Short Calls ($205 strike) - $12M premium at risk if NVDA rallies above $205 by Friday close

- Current price: $192.84

- Needs 6.3% rally to breach strike

- Blackwell production news could trigger gap up

- MRNA Long Calls ($25 strike) - $4.8M positioned for near-term bounce

- Current price: $24.63

- Essentially at-the-money

- Flu vaccine Phase 3 data could be catalyst

- UAN Naked Puts ($120 strike) - $8.4M betting stock stays above $120

- Current price: $120.12 (just $0.12 cushion!)

- Extremely tight margin - corn price moves matter

- Spring planting sentiment key driver

- AMZN Short Calls ($190 strike) - $30M premium collected, deep OTM

- Current price: $245.11

- Safe with 22.5% cushion to strike

- AWS re:Invent unlikely to trigger 22% rally in 10 days

⚠️ RISK WARNING: Short-dated options (1-2 weeks) carry extreme time decay and binary risk. Even "safe" positions can explode if unexpected catalysts emerge. These are NOT positions for beginners.

🎯 Strategic Positioning for Different Investor Types

🎲 For YOLO Traders (1-2% Portfolio Max - EXTREME RISK)

High Conviction Binary Bets:

- MRNA Short Calendar Spread - Fade the November bounce, profit from January call decay

- Entry: Buy back Nov $25 calls ($4.80), keep short Jan $25 calls

- Thesis: Flu vaccine delays extend, stock stays pinned below $25

- Risk: One positive vaccine news = instant loss

- Max Allocation: 1% of portfolio

- UAN Naked Put Sale (Copy the Institution) - Sell Nov 21 $120 puts if confident in fertilizer cycle

- Entry: Sell $120 puts for premium (check current pricing)

- Thesis: Spring planting demand keeps UAN above $120

- Risk: Corn price collapse = forced stock ownership at $120

- Max Allocation: 1-2% of portfolio

⚠️ YOLO WARNING: These trades can result in 50-100% loss of capital allocated. Use stop losses, size appropriately, and NEVER bet rent money on weekly options.

📈 For Swing Traders (3-5% Portfolio)

Technical + Flow Confluence Trades:

- NVDA Diagonal Spread (Reduced Size) - Copy the institutional structure at smaller scale

- Entry: Buy Jan 2026 $195 calls, sell shorter-dated calls at resistance

- Thesis: Blackwell ramp drives gradual rally, collect premium on consolidation

- Setup: Enter on pullbacks to $185-190 support

- Target: $210-220 by January

- Stop: Close below $180

- Position Size: 3% of portfolio

- SLV Synthetic Long (Simplified) - Bullish metals positioning with defined risk

- Entry: Buy June 2026 $35 calls, sell June 2026 $40 puts (or use different strikes)

- Thesis: Fed rate cuts + solar demand + safe haven bid = higher silver

- Setup: Wait for silver consolidation around $33-34

- Target: $40+ by June 2026

- Stop: Exit if silver breaks below $30

- Position Size: 4-5% of portfolio

- ILMN Covered Call Strategy - Sell calls against existing ILMN stock holdings

- Entry: If you own ILMN stock, sell December $120 or January $125 calls

- Thesis: Generate 3-5% monthly income while holding for sequencing growth

- Income: Collect 4-6% annualized premium

- Risk: Called away if stock rips higher (not a bad problem!)

- Position Size: Use existing holdings only

⚠️ SWING TRADER WARNING: Set stop losses at 20-30% of position value. Take profits at 50-75% gains. Don't let winners turn into losers.

💰 For Premium Collectors (Income-Focused, 5-10% Portfolio)

High-Probability Premium Strategies:

- SMCI Covered Calls (Low-Cost Stock Entry) - Sell calls against depressed stock

- Entry: Buy SMCI stock at $30-35, sell $44-50 calls 30-60 days out

- Income: Collect 5-8% monthly premium while stock recovers

- Thesis: Compliance restored, Blackwell demand drives gradual recovery

- Risk: More accounting issues crater stock

- Position Size: 5% of portfolio in stock + calls

- AKAM Vertical Call Spreads - Sell higher strikes, cap upside, collect credit

- Entry: Buy Jan 2028 $115 calls, sell Jan 2028 $130 calls for net credit

- Income: Collect $3-5 net credit per spread

- Thesis: Cloud transformation takes years, cap upside for premium

- Risk: Stock rips above $130, miss extended gains

- Position Size: 5-7% of portfolio

- UAN Cash-Secured Puts - Sell puts on fertilizer stocks at support levels

- Entry: Sell $110-115 puts 30-60 days out, keep cash to cover assignment

- Income: Collect 4-6% monthly premium with willingness to own at lower price

- Thesis: Spring planting demand provides floor under fertilizer names

- Risk: Forced to buy stock if corn prices collapse

- Position Size: 8-10% of portfolio (cash-secured)

⚠️ PREMIUM COLLECTOR WARNING: You're selling insurance - if catastrophe hits, you pay out. Always keep cash reserves, diversify underlyings, and avoid selling naked options without sufficient capital.

🎓 For Entry-Level Option Traders (Learn While Earning)

Educational Trades to Understand Option Flow:

- NVDA Long Call (Single Leg) - Learn basics with liquid mega-cap

- Entry: Buy 1-2 contracts of Jan 2026 $195 or $200 calls (ATM or slight OTM)

- Purpose: Understand time decay, delta, and how institutions use calls

- Thesis: Blackwell ramp drives NVDA higher over next 60 days

- Max Loss: Premium paid ($1,400-2,800 per contract)

- Lesson: Watch how option value changes daily with stock price movement

- Position Size: $500-1,000 maximum (tuition money)

- Paper Trade the AMZN Collar - Simulate without risking capital

- Setup: Use paper trading account to execute collar structure

- Components: Long 1 contract $370 put (Dec 2027) + Short 1 contract $190 call (Nov 21)

- Purpose: Learn how protective puts and covered calls interact

- Lesson: See how the two legs offset each other during market moves

- Position Size: Paper only until you understand mechanics

- Study the CMG Put Spread - Understand disaster hedging

- Action: DON'T TRADE IT - just watch CMG's price action

- Purpose: Learn why institutions buy catastrophic put protection

- Lesson: Track CMG through CEO transition, see if puts pay off

- Takeaway: Understand when hedging is smart vs. wasted premium

📚 BEGINNER EDUCATION PLAN:

- Week 1-2: Study what calls, puts, strikes, and expirations mean

- Week 3-4: Paper trade simple strategies (long calls/puts only)

- Week 5-6: Execute first REAL trade with $500-1,000 max risk

- Week 7-8: Track trade daily, understand P&L swings, learn from mistakes

- Month 2+: Graduate to spreads once you understand single-leg options

⚠️ BEGINNER WARNING:

- 90% of option buyers lose money

- Start with 1-2 contracts maximum

- NEVER trade weeklies as a beginner

- Always know your max loss BEFORE entering

- Use LIMIT ORDERS only (never market orders on options)

📊 Thematic Analysis: What Smart Money Is Really Doing

🛡️ Theme 1: Professional Risk Management Dominates

The Pattern: 6 out of 9 trades involve PROTECTIVE or INCOME-GENERATING strategies, not pure speculation.

- AMZN Collar: Classic hedge of massive long position

- NVDA Diagonal: Long calls funded by short calls

- SMCI Covered Calls: Income generation on depressed stock

- ILMN Covered Calls: Profit-taking after turnaround

- UAN Puts: Premium collection, not naked speculation

- CMG Put Spread: Catastrophe insurance, not bear bet

What This Means: Institutions are NOT aggressively bullish. They're CAUTIOUSLY POSITIONED, hedging upside while protecting downside. This suggests:

- Fear valuations are stretched (AMZN at $300, NVDA at $193, etc.)

- Earnings season / year-end risks warrant protection

- Q4 2025 through Q1 2026 seen as volatile period

- Smart money locking in YTD gains (AMZN +193%, NVDA +201%)

Retail Takeaway: If professionals are hedging after massive runs, maybe you should too. Don't chase all-time highs unprotected.

🤖 Theme 2: AI Infrastructure Hedging (Not Betting)

The AI Plays: NVDA ($62M) + SMCI ($20M) + AKAM ($9.2M) = $91.2M

Notice What's MISSING: These aren't aggressive long calls betting on AI explosion. They're:

- NVDA: Diagonal spread (funded upside, capped by short calls)

- SMCI: Covered calls (selling upside for income)

- AKAM: LEAP roll (extending time, not adding risk)

What This Means: Even in AI stocks, institutions are being DEFENSIVE. No one's betting the farm on continued parabolic moves. The AI trade may be maturing from "buy everything" to "selectively add exposure with risk management."

Retail Takeaway: If you're 100% long AI stocks with no hedges, you're MORE aggressive than billion-dollar funds. Consider taking some profits or adding protective puts.

🥈 Theme 3: Precious Metals Getting Serious Attention

The Surprise: SLV ($63M synthetic long) is the 2nd largest position today.

Why Now?

- Fed rate cuts expected December = lower real rates (bullish for metals)

- Solar demand surge = industrial silver consumption up 15% YoY

- Geopolitical tensions = safe haven bid returning

- Dollar weakness fears = alternative store of value demand

Institutional Structure: They're not buying silver ETF outright - they're constructing SYNTHETIC LONG using options (long calls + short puts). This:

- Reduces capital requirement (collect premium upfront)

- Provides leverage to silver move

- Allows easy exit without moving physical/ETF market

Retail Takeaway: When institutions build 7-month synthetic longs in metals, they're positioning for multi-quarter move, not 1-2 week trade. This is a THEMATIC bet.

💊 Theme 4: Biotech = Contrarian Exits & Turnaround Fades

The Biotech Trades:

- MRNA ($16M): Bearish calendar spread (short the rally)

- ILMN ($12M): Covered call exit (taking profits and leaving)

What This Tells Us:

- MRNA: Institutions don't believe in vaccine pipeline recovery

- ILMN: Turnaround story fully priced at $115, time to exit

Historical Context:

- MRNA was $193 start of year, now $24 (-87%) - institutions SHORTING the bounce

- ILMN was $72 start of year, now $115 (+60%) - institutions EXITING the recovery

Retail Takeaway: Don't try to catch falling knives (MRNA) and don't overstay turnarounds (ILMN). Institutions take profits at rational levels - you should too.

🎯 Weekly & Monthly Expirations Breakdown

🔥 Weekly Options (Expiring November 21, 2025 - 10 Days)

High Risk, High Theta Decay:

| Ticker | Strike | Type | Premium | Current Price | Break-even Risk |

|---|---|---|---|---|---|

| NVDA | $205 | Short Call | $12M | $192.84 | Need 6.3% rally to breach |

| MRNA | $25 | Long Call | $4.8M | $24.63 | Essentially ATM |

| UAN | $120 | Short Put | $8.4M | $120.12 | 0.1% cushion only! |

| AMZN | $190 | Short Call | $30M | $245.11 | Safe (22.5% cushion) |

Weekly Strategy Insight: Institutions use weeklies for INCOME (short calls/puts), not speculation. The premium decay is severe - these options lose 30-50% of value in final week.

📅 Monthly Options (December 2025 & January 2026)

30-60 Day Expirations - Balanced Risk/Reward:

| Ticker | Expiration | Strike | Type | Premium | Strategy |

|---|---|---|---|---|---|

| ILMN | Dec 19, 2025 | $115 | Sell Call | $12M | Covered call exit |

| CMG | Dec 19, 2025 | $37.50 | Long Put | $39M | Disaster hedge (part 1) |

| NVDA | Jan 16, 2026 | $195 | Long Call | $50M | Diagonal long leg |

| MRNA | Jan 16, 2026 | $25 | Short Call | $11M | Calendar short leg |

| SMCI | Jan 16, 2026 | $44 | Sell Call | $20M | Covered call income |

Monthly Strategy Insight: This is the "sweet spot" for most option strategies:

- Enough time for thesis to play out (30-60 days)

- Not paying excessive time premium (like 3-6 month options)

- Liquid enough to adjust or exit if needed

- Institutions favor monthlies for tactical positioning

📊 Quarterly Options (February - March 2026)

90-120 Day Expirations - Intermediate Term:

| Ticker | Expiration | Strike | Type | Premium | Thesis Timeline |

|---|---|---|---|---|---|

| CMG | Feb 20, 2026 | $37.50 | Long Put | $37M | Disaster hedge (part 2) |

| SLV | Jun 18, 2026 | Multiple | Synthetic | $63M | 7-month metals play |

Quarterly Strategy Insight: These capture:

- Full earnings cycles (typically 2 reports)

- Seasonal trends (Q4 holiday → Q1 results)

- Product launch timelines

- Enough time for macro thesis to unfold

🚀 LEAP Options (6+ Months Out)

Long-Term Institutional Positioning:

| Ticker | Expiration | Strike | Type | Premium | Duration |

|---|---|---|---|---|---|

| AMZN | Dec 17, 2027 | $370 | Long Put | $50M | 757 days! |

| SLV | Jun 18, 2026 | Multiple | Synthetic | $63M | 217 days |

| AKAM | Jan 21, 2028 | $115 | Long Call | $9.2M | 802 days! |

LEAP Strategy Insight:

- Only 3 of 9 trades are LEAPs (>6 months)

- Used for STRATEGIC themes (AWS dominance, CDN transformation, metals cycle)

- NOT for tactical trading - these are "set and forget" positions

- Institutions willing to pay time premium for long-term conviction plays

Key Takeaway: Notice the mix - 4 weekly/monthly (tactical), 2 quarterly (intermediate), 3 LEAPs (strategic). Professionals use DIFFERENT timeframes for DIFFERENT purposes. Retail often makes mistake of trading everything short-term.

📅 Catalyst Calendar: Events That Will Move These Positions

This Month (November 2025)

| Date | Event | Ticker Impact | Expiration Relevance |

|---|---|---|---|

| Nov 21, 2025 | OPTIONS EXPIRATION | NVDA, MRNA, UAN, AMZN short calls expire | CRITICAL for weekly positions |

| Nov 30 - Dec 5 | AWS re:Invent Conference | AMZN cloud strategy updates | Post short-call expiration |

Next Month (December 2025)

| Date | Event | Ticker Impact | Expiration Relevance |

|---|---|---|---|

| Dec 18, 2025 | Fed Rate Decision | SLV (precious metals sensitive to rates) | Mid-cycle for June expiry |

| Dec 19, 2025 | OPTIONS EXPIRATION | ILMN covered calls, CMG puts (part 1) | Monthly expiration |

| Dec 2025 | Nasdaq Compliance Deadline | SMCI must maintain compliance or face delisting | Pre-January expiration |

Q1 2026 (January - March)

| Date | Event | Ticker Impact | Expiration Relevance |

|---|---|---|---|

| Jan 13-16, 2026 | JPM Healthcare Conference | ILMN sequencing updates, MRNA pipeline news | Post-December expiration |

| Jan 16, 2026 | OPTIONS EXPIRATION | NVDA, MRNA, SMCI monthlies expire | MAJOR monthly expiry |

| Feb 20, 2026 | OPTIONS EXPIRATION | CMG disaster hedges (part 2) expire | Final disaster protection |

| Feb 2026 | Q4 Earnings Season | AKAM, ILMN, SMCI report Q4 results | Between January & February expiries |

| Q1 2026 | NVDA Q4 FY2025 Results | Blackwell revenue confirmation ($11B expected) | Pre-January expiration |

Mid-2026 & Beyond

| Date | Event | Ticker Impact | Expiration Relevance |

|---|---|---|---|

| Jun 18, 2026 | OPTIONS EXPIRATION | SLV synthetic long expires | 7-month metals thesis conclusion |

| Q2 2026 | Spring Planting Season | UAN fertilizer demand peak | Long past November expiry |

| Jan 21, 2028 | OPTIONS EXPIRATION | AKAM LEAPs expire (802 days out!) | Ultimate long-term transformation bet |

| Dec 17, 2027 | OPTIONS EXPIRATION | AMZN protective puts expire (757 days!) | Multi-year AWS hedge conclusion |

💡 Risk Management Principles: Learn from the Professionals

⚠️ CRITICAL WARNING: Don't Blindly Copy These Trades

Why Professional Trades Don't Translate to Retail:

- Size Matters: Institutions are hedging $100M+ positions. You're trading $5,000. The RELATIVE impact is totally different.

- Tax Treatment: Funds have different tax treatment on options (wash sales, mark-to-market, etc.). Your P&L calculus is different.

- Risk Tolerance: Losing $40M on a hedge is "cost of insurance" to a billion-dollar fund. Losing $4,000 might be your rent money.

- Time Horizon: Institutions can wait 757 days for AMZN puts to pay off. Can you afford to have capital tied up for 2+ years?

- Portfolio Context: The AMZN collar makes sense if you own $656M of Amazon stock. Do you? If not, the trade logic breaks down completely.

🎯 How to Actually USE This Intelligence

DO:

- ✅ Understand the THESIS (why institutions positioned this way)

- ✅ Learn the STRUCTURE (how multi-leg strategies work)

- ✅ Note the TIMING (when they expect catalysts)

- ✅ Adapt the CONCEPT to your size and risk tolerance

- ✅ Use stops and position limits religiously

DON'T:

- ❌ Copy the exact trade at your account size

- ❌ Assume institutions are always right

- ❌ Ignore your own risk parameters

- ❌ Trade without understanding the structure

- ❌ Use weekly options as a beginner

🛡️ Position Sizing Rules by Experience Level

Entry Level Traders:

- Max 2-3% of portfolio in any single option position

- Start with 1-2 contracts only

- Use monthlies (30-60 days), avoid weeklies

- Stick to liquid names (NVDA, AMZN, etc.)

- Paper trade for 1-2 months before risking real capital

Intermediate Traders:

- Max 5-7% of portfolio in any single position

- Can use 3-5 contracts

- Mix of weeklies (1-2%) and monthlies (3-5%)

- Understand Greeks (delta, theta, vega)

- Have at least 6-12 months of profitable option trading

Advanced Traders:

- Max 10-15% in concentrated positions

- Can scale to 10-20 contracts (or more with proper capital)

- Use all timeframes strategically

- Manage portfolio-level Greeks

- Track performance for 2+ years with audited results

⚠️ UNIVERSAL RULE: If a single option position losing 100% would materially impact your life (rent, bills, etc.), you're sized TOO LARGE. Cut position size by 50-75%.

⏰ The Patience Principle

Why Most Retail Traders Lose Money:

They try to turn $5,000 into $50,000 in 1 month using weekly options. The math:

- Need 10x return = 900% gain

- Requires stock to move 15-20% in RIGHT DIRECTION within DAYS

- Probability of success: ~2-5%

- Probability of total loss: ~80-90%

How Professionals Actually Make Money:

They compound 5-10% monthly gains over YEARS:

- Collect $12M premium selling NVDA calls

- Generate 3-5% monthly income on covered calls

- Hedge massive positions for "cost of insurance"

- Take profits systematically (ILMN at +60%, not holding for +200%)

The Retail Path to Success:

- Target 3-5% monthly gains consistently

- Use stop losses to prevent 20-30% losses

- Take profits at 50-75% (don't wait for 10-baggers)

- Compound over 12-24 months

- $5,000 compounded at 3% monthly = $10,150 after 12 months (102% gain with MUCH lower risk than chasing 10-baggers)

📊 Complete Analysis Directory

Premium Institutional Analyses (Full Deep Dives):

🔥 Largest Flows:

- AMZN: $80M Protective Collar Strategy

- SLV: $63M Synthetic Long Stock

- NVDA: $62M Diagonal Call Spread

- CMG: $39M Catastrophic Put Hedge

💰 Medium Flows:

🎯 Smaller Strategic Flows:

⚠️ RISK DISCLOSURE

IMPORTANT LEGAL DISCLAIMERS:

Not Financial Advice: This newsletter is for educational and informational purposes only. It is NOT personalized investment advice, a recommendation to buy/sell specific securities, or a solicitation of any kind.

Option Trading Risks:

- Options can expire worthless, resulting in 100% loss of premium paid

- Selling options (short positions) can result in UNLIMITED losses

- Weekly options carry extreme time decay risk (theta)

- Leverage magnifies both gains AND losses

- Most retail option traders lose money over time

Performance Disclaimers:

- Past institutional trades do not guarantee future results

- Large option flows can be hedges, arbitrage, or positioning - not directional bets

- Institutions have different risk profiles, time horizons, and tax treatment than retail traders

- Copying professional trades at retail size often fails due to structural differences

Do Your Own Research:

- Verify all facts and figures independently

- Understand the mechanics of any strategy before trading

- Consult a licensed financial advisor for personalized guidance

- Never trade with money you can't afford to lose

- Start small, paper trade first, and scale gradually

Accuracy Disclaimer: While we strive for accuracy, option flow data can be incomplete, misclassified, or reported with delays. Always verify trade details and current market conditions before acting.

No Guarantees: There are NO guaranteed profits in option trading. Anyone claiming guaranteed returns is lying. Approach all claims with skepticism.

📧 Questions, Feedback, or Issues? Reply to this newsletter or email: support@ainvest.com

Stay sharp. Trade smart. Manage risk.